AppLovin: The Advertising Platform Silicon Valley Filed Away

- Sia Gholami

- /

- June 10, 2026

In 2012, Adam Foroughi tried to raise $1 million for AppLovin at a $4 million valuation. He later said he would have given up a quarter of the company for that money. The top venture firms passed.[1]

It was not an irrational rejection. AppLovin was entering mobile advertising, a crowded and unglamorous market already shaped by Google, Facebook, Apple, and a long list of mobile ad networks. The company did not have a famous consumer app. It did not have the mythology of a social network or the technical glamour of a deep-infrastructure startup. It had a strange name and a practical pitch: mobile app developers needed a better way to find users.

Foroughi later recalled the investor reaction with a phrase that captured the skepticism: why would a “goofy name little company” be able to compete with Google, Facebook, and Amazon?[1]

The name was not the real reason VCs passed; the category was. But the name created a longer-running problem. It kept causing the market to misfile the company even as the business outgrew its original description. AppLovin sounded like a mobile-app vendor. The later shift toward the Axon brand gave the company a cleaner way to describe what it had actually become: not app marketing in the narrow sense, but an AI-powered system for matching advertisers with high-intent users across a massive mobile-game network. The rebrand was as much about investor and advertiser perception as it was about product.

What investors missed in 2012 was that AppLovin was not trying to build the next Facebook, Google, or TikTok. It was building a performance system in a part of mobile advertising where the winner would be decided by math: if advertisers could spend one dollar and make more than one dollar back, the budgets would follow.

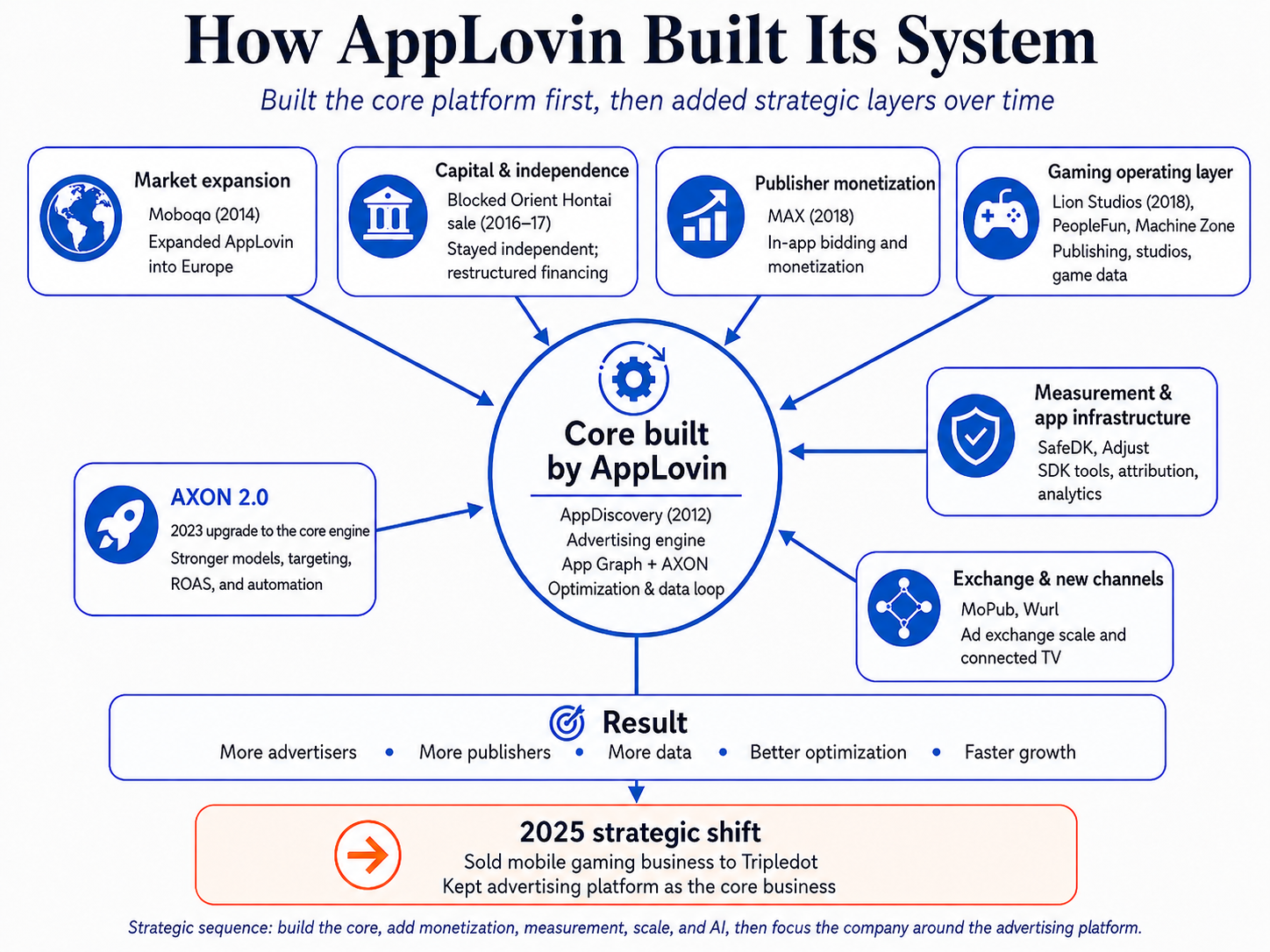

The first product

The company’s first product, AppDiscovery, launched on Android and iOS in 2012. It helped developers acquire users for their apps. The product sat at the center of a fast-growing problem. The app stores had made distribution global, but they had also made discovery brutal. Anyone could publish a game or app; very few could profitably scale one.[2]

Without venture backing, AppLovin had to prove the economics early. Foroughi has said the ad platform launched in March 2012, reached roughly $1 million a month in run-rate revenue by November, and was slightly profitable. AppLovin’s IPO filing later said the company had positive operating cash flow from operating activities every year since 2013.[1][2]

That early constraint became part of the operating model. AppLovin did not start as a company optimized for headcount, brand, or fundraising momentum. It was optimized for campaigns that worked.

Nearly sold

In September 2016, the company agreed to sell a majority stake to Orient Hontai Capital, a China-linked private-equity investor, in a transaction valued around $1.4 billion. For a company built with little early outside capital, it looked like a major outcome. Then the Committee on Foreign Investment in the United States intervened. After more than a year of regulatory scrutiny, the deal was abandoned in November 2017 and restructured as $841 million in debt financing, leaving AppLovin independent and with access to capital rather than a change of control.[3]

In hindsight, the blocked sale became one of the most important accidents in the company’s history. Had the transaction closed as planned, AppLovin might have become a controlled asset inside someone else’s portfolio. Instead, it kept its independence at the moment mobile advertising and mobile gaming were entering a much larger cycle. Foroughi later put the outcome more bluntly: “CFIUS saved my ass.”[4]

Building the system

The next phase was assembly. KKR invested $400 million in AppLovin in 2018, reportedly valuing the company at about $2 billion. That same year, AppLovin launched Lion Studios, a mobile game publishing arm, and acquired MAX, an in-app bidding and monetization platform.[5][6][7]

MAX mattered because it put AppLovin closer to the publisher side of the mobile-app economy. AppDiscovery helped advertisers acquire users. MAX helped publishers monetize inventory. Lion Studios gave AppLovin a closer view of how mobile games were published, marketed, and scaled. AppLovin was no longer only selling user acquisition. It was building around the full lifecycle of mobile app growth.

Over time, MAX also became one of AppLovin’s most important strategic assets. Industry analyses have estimated that MAX holds a majority share among top ad-monetized mobile games, making it a central gateway between publishers, advertisers, and the behavioral signals that feed AppLovin’s advertising models.[8]

Alongside MAX, AppLovin also acquired Moboqo for European market access, PeopleFun and Machine Zone for gaming operations, SafeDK for SDK management, Adjust for measurement and attribution, MoPub from Twitter for $1.05 billion to add mobile exchange scale, and Wurl to extend toward connected TV. Each deal gave AppLovin another layer around the same core problem: helping advertisers find users and helping publishers monetize attention.[9][10][11][12]

From the outside, the company could look hard to categorize: ad network, game publisher, monetization platform, analytics provider, exchange operator. Internally, the pieces pointed in one direction. AppLovin was tightening the loop between advertisers, publishers, app activity, measurement, and optimization.

Gaming was central to that system, but it was not the endpoint. Mobile games generate enormous volumes of impressions, installs, purchases, and behavioral signals. They also discipline advertising quickly. A campaign either produces valuable users or it does not. A game either monetizes or it fades. That made gaming a useful proving ground for a performance-advertising platform.

Central to the system, even before the IPO, was AXON, the machine-learning recommendation engine that powered AppDiscovery and used AppLovin’s App Graph to improve ad matching and monetization. It was not a later acquisition or a final layer. It was part of the core system that the surrounding acquisitions ultimately strengthened.[2]

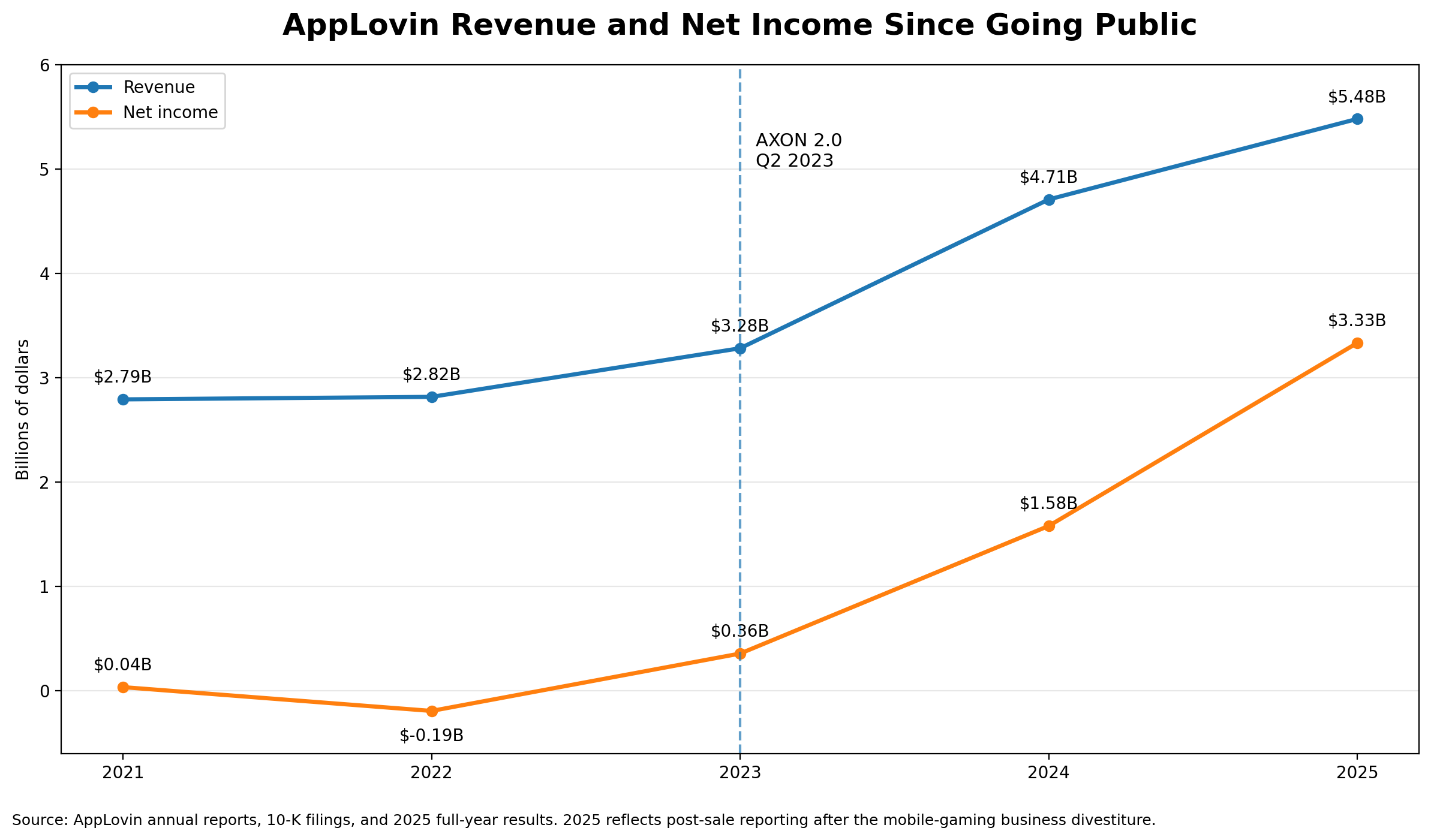

The scale AppLovin brought to its IPO reflected that. Revenue had grown from $483 million in 2018 to $994 million in 2019 and $1.45 billion in 2020, a 76% compound annual rate from 2016 to 2020, according to AppLovin’s own IPO filing. The company went public in April 2021.[2]

The AXON inflection

The clearer milestone came in 2023. AppLovin released AXON 2.0 in the second quarter, and management credited the upgraded engine with stronger campaign performance.[13]

The shift did not show up as a sudden spike in total revenue. It showed up first in the business mix. Advertising revenue rose from $1.05 billion in 2022 to $1.84 billion in 2023, while total revenue rose from $2.82 billion to $3.28 billion. By 2024, the mix shift had become much harder to miss: advertising revenue reached $3.22 billion, total revenue reached $4.71 billion, and net income jumped to $1.58 billion.[14]

What the revenue figures alone understate is the margin trajectory. AppLovin’s advertising segment ran at adjusted EBITDA margins around 69% in 2023, rising to approximately 73% to 78% through 2024, as the cost base stayed relatively fixed while revenue compounded. The games segment, by contrast, ran margins in the mid-to-high teens over the same period. The story of 2023 and 2024 was not just that advertising grew fast; it was that each incremental dollar of advertising revenue converted to profit at a rate the games business could not approach.[14]

AppLovin reported $5.48 billion of revenue and $3.33 billion of net income for 2025.[15]

From games to software

For years, AppLovin looked like a mobile-gaming company. That was partly true, but incomplete.

Gaming was both a business line and a proving ground. By owning and publishing games, AppLovin could see the entire lifecycle of a mobile app: development, launch, user acquisition, monetization, retention, and scaling. That knowledge fed back into its advertising systems.

But there was a tension. Game development is creative, hit-driven, and operationally messy. Advertising software is scalable, automated, and margin-rich. AppLovin used games to help build the machine, but the machine eventually became more valuable than the games.

That is why the Tripledot sale mattered. In 2025, AppLovin sold its mobile gaming business to Tripledot Studios for $400 million in cash plus equity representing roughly 20% of Tripledot’s fully diluted shares at closing. AppLovin did not leave gaming advertising; gaming remained part of the ecosystem. What it exited was direct ownership of the game portfolio. The company kept the higher-margin advertising platform at the center and retained upside in the buyer.[16]

The shift made AppLovin easier to understand and harder to dismiss. The business was no longer a hybrid of software and owned games. It was increasingly a lean, AI-driven advertising company with unusually high operating leverage.

The lean company

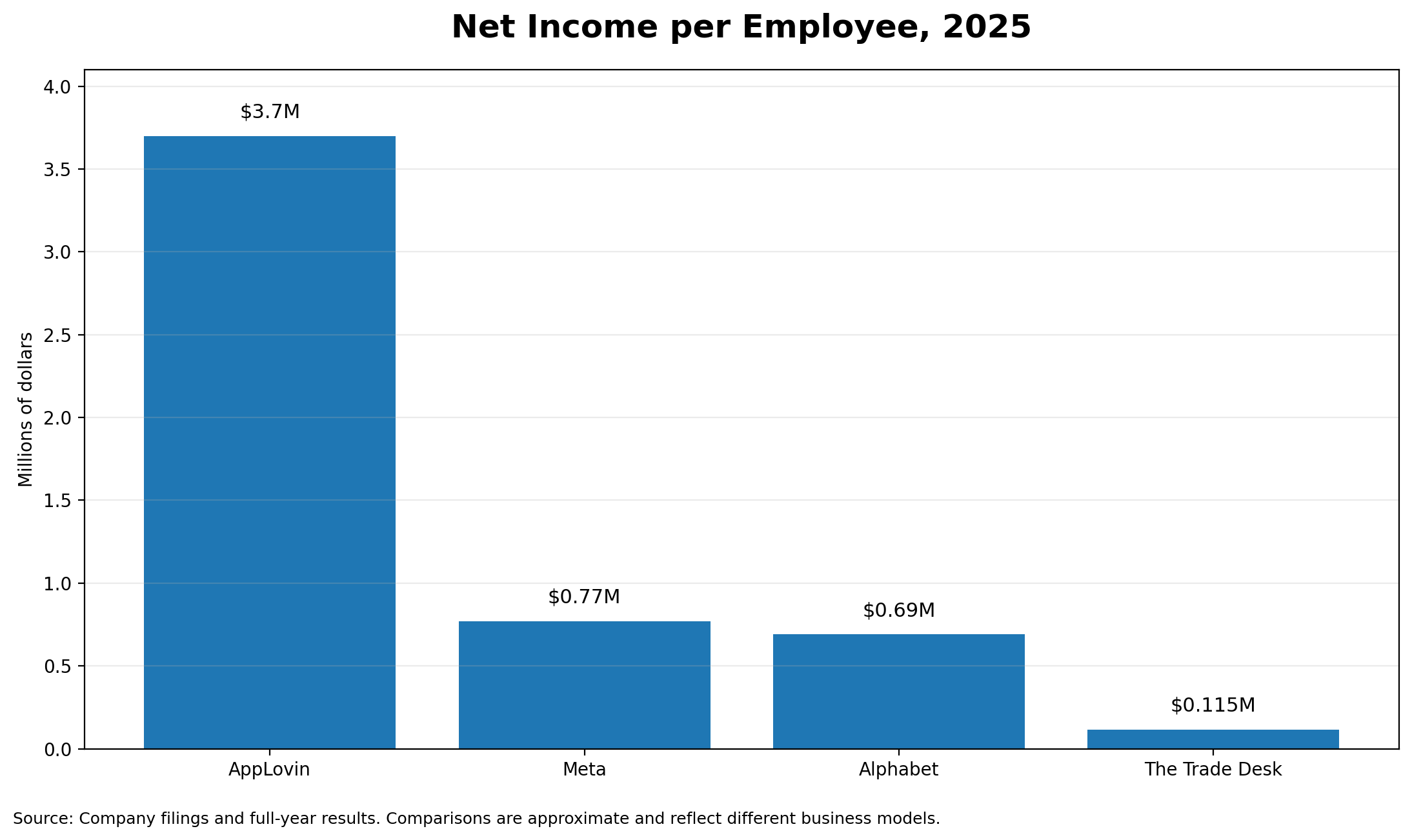

That operating leverage is clearest in headcount. AppLovin reported 898 employees at the end of 2025, across 15 countries, with about 60% outside the United States. The company described its structure as lean, built around leveraging technology wherever possible.[15]

Foroughi has made the same point more directly. He has argued that with AI tools, one exceptional person can be as powerful as 10, 20, 50, or even 100 people. That philosophy shows up in the numbers. AppLovin generated approximately $3.7 million of net income per employee in 2025, roughly five times Meta’s $770,000, five times Alphabet’s $690,000, and 30 times The Trade Desk’s $115,000.[1][15][17][18][19]

The comparison is imperfect. Meta and Alphabet carry large workforces in hardware, data centers, and content moderation, while The Trade Desk runs a more sales-intensive model. But the gap still captures something important: AppLovin’s model is unusually efficient.

The same efficiency also creates risk. AppLovin’s advertising systems, AXON model architecture, publisher relationships, and ecommerce expansion are being managed by an unusually small team. A company of this scale operating with fewer than 900 employees has less redundancy if key talent departs, if a critical system fails, or if expansion outpaces the organization’s ability to execute.

The moat question

AppLovin’s financial performance has been striking enough that a natural question follows: why can’t someone replicate it?

The honest answer is that replication would require assembling several things simultaneously. AXON is trained on data that flows through MAX, the in-app bidding platform that sits between publishers and advertisers across a large portion of the mobile gaming ecosystem. That data includes not just ad impressions but post-install behavior: what users do after they download an app, how they spend, how they retain, and how those patterns vary across device types, geographies, and game genres. A competitor trying to build a rival model would need comparable data scale, and that data can only be accumulated by operating a similar publisher network over a similar period of time.

The flywheel compounds this. More publishers on MAX means more behavioral signal flowing into AXON. Better signal improves targeting accuracy. Better targeting improves advertiser ROAS. Higher advertiser ROAS attracts more spend. More spend means more publisher revenue, which attracts more publishers. Each rotation of that loop makes it marginally harder for an entrant to start.

The durability of that advantage is a genuine open question, however. Unity’s LevelPlay platform is a direct competitive response, and industry observers have noted meaningful performance improvements from Unity, Moloco, and Mintegral through 2025. Google and Meta each have structural data advantages in their own ecosystems that AppLovin cannot access directly. And the moat depends in part on AppLovin continuing to be sufficiently dominant in mobile gaming supply, a position that weakens if publishers diversify their mediation stacks or if Apple and Google further restrict the cross-app behavioral signals that feed AXON’s models. The infrastructure advantage is real, but it is not impenetrable.[8][20][21]

Ecommerce and Axon Ads Manager

The company’s ecommerce push starts from an unusual position. AppLovin already has scale, with a network reaching more than a billion daily active users through targeted ads in mobile games. The question is not whether AppLovin has a large surface area. It does. The question is whether it can persuade advertisers outside gaming to treat that surface as premium performance inventory.[22]

That is harder than it sounds. Many ecommerce brands know Meta, Google, TikTok, Amazon, and Pinterest. Far fewer built their media plans around AppLovin. For years, AppLovin’s name carried the wrong associations for the broader market: mobile apps, games, and adtech plumbing. Axon gave the company a product identity that sounded closer to the business it was trying to become: AI-driven performance advertising, real-time bidding, and measurable return.

The rollout reflected that challenge. In 2024, AppLovin began bringing ecommerce advertisers onto the platform in a limited way. In October 2025, it rebranded its customer-facing advertising platform around Axon and launched Axon Ads Manager on an invite-only, referral basis. By December 2025, roughly 5,300 ecommerce clients had been onboarded.[23][24]

AppLovin’s ad experience is different from what most ecommerce marketers run on Meta or TikTok. Axon ads are mobile-first and immersive: full-screen vertical video, followed by an interactive page and, for shopping advertisers, often a dynamic product-catalog view. AppLovin’s own support documentation says the video component can be unskippable for up to 60 seconds, and that advertisers should diversify creatives to test different styles and messages.[25]

That creates a creative bottleneck. Gaming advertisers are used to producing large volumes of videos, playable ads, end cards, and rapid creative tests. Many ecommerce brands are not. A mistake would be to take the same assets built for Meta or TikTok, upload them to Axon, and expect the platform to behave the same way. The format asks for different creative muscle. Zacks research citing AppLovin’s own data reported in early 2026 that roughly 57% of qualified ecommerce leads who enter the onboarding process ultimately go live, a figure that points directly at this creative friction as a meaningful constraint on near-term scaling.[26]

AppLovin appears to understand that. As it prepared to open Axon more broadly in 2026, the company also began rolling out AI-powered creative tools and self-serve infrastructure. Foroughi told investors that, after 14 years as a closed platform, advertisers around the world would be able to sign up for Axon and start running campaigns. He also described a system where an advertiser could onboard, generate high-performing ads, and scale campaigns profitably without needing to talk to a human. General availability was targeted for the first half of 2026.[26]

The social-media ambition

After years of adding layers around mobile advertising, including games, monetization, measurement, exchange scale, and creative tools, AppLovin’s interest in social media represented a more ambitious step: moving closer to the attention layer itself.

In 2025, the company made an unexpected bid to acquire TikTok’s assets outside China. The idea looked strange only if AppLovin was still viewed as a mobile-gaming ad company. Seen through the lens of its advertising system, the logic was clearer. AppLovin had spent more than a decade learning how to monetize mobile attention. TikTok had one of the largest pools of mobile attention in the world.

Foroughi argued that AppLovin could improve TikTok’s monetization and help address concerns around data and algorithmic control. The bid failed. TikTok’s U.S. restructuring ultimately moved forward through a joint venture backed by Oracle, Silver Lake, and MGX.[27][28]

AppLovin’s interest in social media did not disappear. In 2026, the company quietly launched Gist, a referral-code social app with photo carousels, videos, mini-games, and interest-based feeds. A social product gives AppLovin a chance to own more of the attention surface itself: content, creators, social signals, commerce intent, and ad inventory, another potential source of data and monetizable traffic for AXON.[27]

But social media is not just an ad-optimization problem. It requires culture, creator liquidity, content moderation, trust, and habit formation. AppLovin had also publicly backed Flip, a social commerce platform, with a $50 million investment in 2024. The venture later shut down, a reminder that consumer social products can burn capital quickly without creating durable habits. AppLovin has shown it can build unusually profitable advertising infrastructure. It has not yet shown it can build a consumer social network.[29][30]

Risks

AppLovin operates in advertising, AI, privacy, app-platform rules, measurement, and automated targeting. Its own filings warn that changes by third-party platforms, regulation, competition, and privacy rules could hurt the business.[14][15]

Between February and March 2025, three short-seller firms, Fuzzy Panda, Culper Research, and Muddy Waters, published reports making overlapping but distinct allegations. Fuzzy Panda argued that AXON’s reported ROAS was built on deceptive advertising tactics and called the platform “the nexus of a House of Cards.” Culper’s specific claim was that AppLovin exploited app permissions to push silent, backdoor app installations onto users’ devices, effectively generating install events without clear user consent. Muddy Waters alleged that AppLovin “systematically” violated the terms of service of Meta, Snap, TikTok, Reddit, and Google by impermissibly extracting proprietary user identifiers to build cross-platform targeting profiles through a technique known as identifier bridging or fingerprinting.[31][32][33]

AppLovin denied the claims in detail. Foroughi publicly called the reports false and misleading, retained outside counsel, and argued that critics either misunderstood the technology or were acting in bad faith. He noted the reports appeared immediately after an earnings period during which AppLovin was restricted from responding with financial performance.[31][32][33]

In October 2025, Bloomberg reported that the SEC’s Cyber and Emerging Technologies Unit had opened an investigation into AppLovin’s data-collection practices, following an alleged whistleblower complaint and the earlier short-seller reports. The specific focus, according to people familiar with the matter, was whether AppLovin violated platform partners’ service agreements to push more targeted advertising to consumers. AppLovin said it regularly engages with regulators and would disclose material developments through appropriate channels. The investigation remained open as of mid-2026.[34][35][36]

The regulatory risk goes beyond any single probe. Apple has banned fingerprinting, and Google has moved to restrict similar techniques. If AXON’s data collection is constrained by platform policy changes or regulatory action, the signal quality feeding the model degrades, and with it, the advertiser ROAS that drives budget allocation to the platform. That is the bear case in its sharpest form: not that AXON does not work, but that the data practices enabling it may not be sustainable at current scope.[37][38]

Where the debate sits

The bull and bear cases are genuinely in tension, and neither is obviously wrong.

The bull case rests on the compounding nature of the data flywheel, the demonstrated ability to expand into new verticals, and the high-margin, relatively fixed-cost structure of the advertising platform. If AXON continues to deliver measurable ROAS advantages and ecommerce advertisers scale their spend, the unit economics argue for continued revenue growth with expanding margins. The self-serve general availability in 2026 is the key catalyst: if it significantly widens the advertiser base, the addressable market expands well beyond mobile gaming.

The bear case centers on three specific vulnerabilities. First, regulatory and platform risk: if Apple, Google, or the SEC materially constrain AppLovin’s data collection methods, AXON’s targeting precision erodes. Second, competitive catch-up: the gap between AXON and rivals like Unity’s LevelPlay, Moloco, and eventually Meta or Google’s own mobile-first products is real but not permanent. Third, ecommerce execution: the 57% go-live rate on qualified leads suggests a meaningful creative onboarding problem that may be slow to fix, and any sustained disappointment in ecommerce ROAS would slow the vertical expansion the growth story depends on.

Conclusion

The company began as a mobile-ad startup that top VCs passed on at a $4 million valuation. It built a strong core in app discovery and performance advertising, survived a blocked sale, and then used capital to add the missing layers around its platform: monetization, measurement, exchange scale, gaming operations, and more powerful AI optimization.

The distinguishing factor was not AXON alone. It was AXON inside a system AppLovin had spent years assembling.

AppLovin built the core engine, then added the infrastructure around it. It launched Lion Studios. It bought MAX. It added Adjust, MoPub, SafeDK, Wurl, PeopleFun, and Machine Zone. It sold the mobile gaming business. It kept the advertising platform.

As AXON improved, the story shifted from games to software and from a niche mobile-ad company to one of the higher-margin advertising platforms in the public market.

The risk the market now faces is the mirror image of the mistake it made in 2012. Then, analysts underestimated AppLovin by assuming the category defined the ceiling. Now, the question is whether assuming that what worked so powerfully inside mobile gaming will translate with equal force into every adjacent market. Performance advertising is less loyal to categories than to results. The ecommerce and social chapters are still being written.

AppLovin did not look like a platform-scale business when it started. It looked like a small company in a crowded corner of advertising. But the market was looking at the category, not the system. AppLovin’s advantage was not that mobile advertising suddenly became glamorous. It was that the company had built a feedback loop between advertisers, publishers, data, and machine learning that became harder to copy as it scaled.

That was the business hiding behind the strange name.

References

- David Senra, “Adam Foroughi,” Founders Podcast interview transcript. Used for the fundraising anecdote, “goofy name little company” quote, early profitability comments, and Foroughi’s productivity comments.

- AppLovin, Form S-1 Registration Statement, 2021. Used for AppDiscovery timing, positive operating cash flow language, pre-IPO revenue figures, 2016 to 2020 CAGR, AXON, and App Graph.

- AppLovin and public transaction reporting on the Orient Hontai transaction. Used for the September 2016 majority-stake agreement, $1.4 billion valuation, CFIUS review, November 2017 abandonment, and $841 million debt-financing restructuring.

- Business Insider profile of Adam Foroughi. Used for the “CFIUS saved my ass” quote, reported from the Jefferies Private Growth Conference.

- KKR announcement and related reporting on its 2018 investment in AppLovin. Used for the $400 million investment and reported valuation.

- AppLovin announcement on Lion Studios, 2018. Used for the launch of Lion Studios as a mobile game publishing arm.

- AppLovin reporting and acquisition coverage on MAX, 2018. Used for the acquisition of MAX as an in-app bidding and monetization platform.

- GameBiz Consulting, 2025 mobile-game mediation analysis. Used for the claim that MAX holds a majority share among top ad-monetized mobile games, including estimated mediation share among top-downloaded and top-grossing ad-monetized game samples.

- AppLovin reporting on Moboqo. Used for the 2014 acquisition and European market-access point.

- AppLovin reporting on PeopleFun, Machine Zone, SafeDK, and Adjust. Used for gaming operations, SDK management, and measurement and attribution points.

- AppLovin announcement on MoPub acquisition from Twitter. Used for the $1.05 billion transaction and mobile exchange-scale point.

- AppLovin announcement on Wurl acquisition. Used for the connected-TV expansion point.

- AdExchanger, 2023 report on AppLovin’s AXON 2.0 release and second-quarter outperformance. Used for the AXON 2.0 milestone.

- AppLovin 2024 Form 10-K and quarterly shareholder letters filed with the SEC. Used for 2022 to 2024 total revenue, advertising revenue, net income, segment adjusted EBITDA margins, and risk-factor discussion.

- AppLovin 2025 full-year financial results and annual-report materials. Used for 2025 revenue, net income, employee count, international workforce mix, and lean-organization language.

- AppLovin announcement on the sale of its mobile gaming business to Tripledot Studios. Used for the $400 million cash consideration and approximately 20% equity stake in Tripledot at closing.

- Meta 2025 annual-report materials. Used for employee count and net income per employee comparison.

- Alphabet 2025 annual-report materials. Used for employee count and net income per employee comparison.

- The Trade Desk 2025 annual-report materials. Used for employee count and net income per employee comparison.

- GameMakers, December 2025 analysis. Used for competitive dynamics around Unity, Moloco, Mintegral, LevelPlay, and mobile-game monetization.

- Klover.ai, July 2025 analysis. Used for discussion of MAX, publisher lock-in, mediation, and competitive dynamics.

- Axon and AppLovin product materials. Used for the claim that AppLovin reaches more than a billion daily active users through targeted ads in mobile games.

- Modern Retail reporting on AppLovin’s October 2025 Axon rebrand and invite-only Axon Ads Manager launch.

- AlphaR&D Insights analysis of AppLovin data. Used for the approximately 5,300 ecommerce-client figure by December 2025.

- AppLovin support documentation on Axon ad formats. Used for full-screen video, interactive pages, product-catalog views, unskippable video up to 60 seconds, and creative-testing requirements.

- Zacks/TalkMarkets reporting on AppLovin data, March 2026. Used for the 57% go-live rate for qualified ecommerce leads and the first-half 2026 general-availability target.

- Business Insider reporting on AppLovin’s TikTok bid and Gist launch.

- Associated Press reporting on the TikTok U.S. joint-venture outcome backed by Oracle, Silver Lake, and MGX.

- AppLovin April 2024 announcement of a $50 million investment in Flip’s Series C.

- Business Insider reporting on Flip’s later shutdown.

- CNBC coverage of Fuzzy Panda and Culper Research short-seller claims and AppLovin’s response, February 2025.

- Marketing Brew coverage of AppLovin short-seller allegations and company responses, February and March 2025.

- The Register coverage of Muddy Waters’ March 2025 AppLovin short report and AppLovin’s response.

- Bloomberg, October 6, 2025 report on the SEC investigation into AppLovin’s data-collection practices.

- National Law Review coverage of the SEC investigation and related legal/regulatory context.

- Robinson+Cole coverage of the SEC investigation and data-practices issues.

- Apple developer and privacy-policy materials on fingerprinting restrictions.

- Google privacy and platform-policy materials on restrictions affecting fingerprinting and cross-app identifiers.

About The Author

Sia Gholami

Sia Gholami is a distinguished expert in the intersection of

artificial intelligence and finance. He holds a bachelor's, master's, and Ph.D. in computer

science, with his doctoral thesis focused on efficient large language models and their

applications, an area crucial to the development of advanced AI systems. Specializing in machine

learning and artificial intelligence, Sia has authored several research papers published in

peer-reviewed venues, establishing his authority in both academic and professional circles.

Sia has created AI models and systems specifically designed to identify opportunities in the

public market, leveraging his expertise to develop cutting-edge financial technologies. His most

recent role was at Amazon, where he worked within Amazon Ads, developing and deploying AI and

machine learning models to production with remarkable success. This experience, combined with

his deep technical knowledge and understanding of financial systems, positions Sia as a leading

figure in AI-driven financial technologies. His extensive background has also led him to found

and lead successful ventures, driving innovation at the convergence of AI and finance.